Why Do Mortgage Rates Increase?

Mortgage rates fluctuate over time as a result of the interaction of the supply and demand for money in the economy. These changes affect the interest rate lenders charge prospective homeowners. By tracking the economic developments that influence mortgage rates, home buyers can understanding how these rates are determined.

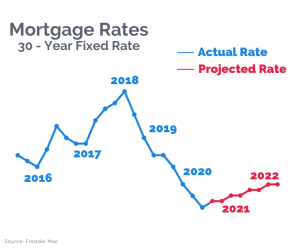

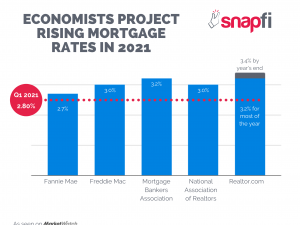

Most experts agree: we saw the historical bottom of the rates back in late 2020 / early 2021, and they are expected to go back up while the economy and housing market stabilizes post COVID-19 pandemic.

Should you refinance or purchase at this time?

Request a quote in 3 mins, no hard credit pull needed:

As rates are expected to increase, it may be a good time to consider what factors make rates go up:

Federal Reserve Board

Economic activity is measured nationally to determine the appropriate interest rate. The Federal Reserve Board, which is the central banking authority in the United States, measures economic growth through 12 Federal Reserve branches across the country. Federal Reserve branches collect economic information from their respective regions and report to the Federal Reserve Board during regular meetings in Washington, D.C. The outcome of this meeting determines whether the Federal Reserve will try to increase interest rates to control growth or decrease rates to spark growth and encourage borrowing.

Benchmarks

In addition to regular monitoring by the federal government, the financial markets establish benchmarks to understand where interest rates might be headed. The yield on the 10-year treasury bond is widely considered to be a benchmark for long-term mortgage interest rates. As a result, lenders often tie mortgage rates to the 10-year treasury bond to keep the mortgage loan profitable in the long run. Any changes in the 10-year treasury bond yield influence how mortgage rates are set for current mortgages.

Should you buy, cash out, or refinance at this time? It all comes down to dollars and cents.

Use our calculator or request a quote to see how much more we can leave in your pocket: